‘The Sound of Music,” the hit Broadway musical and later film, includes a scene in which a group of Austrian nuns, in the days leading up to the start of World War II, sing a song titled “How Do You Solve a Problem Like Maria?” Maria, played by Julie Andrews in the film, is a well-liked novice, but she has had some trouble fitting into the regime of the cloistered convent life. The problem is resolved when Maria takes a leave to think about her vocation, assuming a job as a governess of the von Trapp family.

Like the Austrian nuns, many countries in the euro zone, particularly Portugal, Ireland, Italy, Greece and Spain—together dubbed the PIIGS by The Economist—are adapting the titular question of that famous song to another problem: the euro. There are plenty of reasons not to sing, but rather sigh, and sigh deeply, or perhaps sing the blues. In 2012, a little more than a decade after the introduction of the euro, we see marked divergence between the economic performance of the PIIGS and that of the country at the center of the euro zone, Germany.

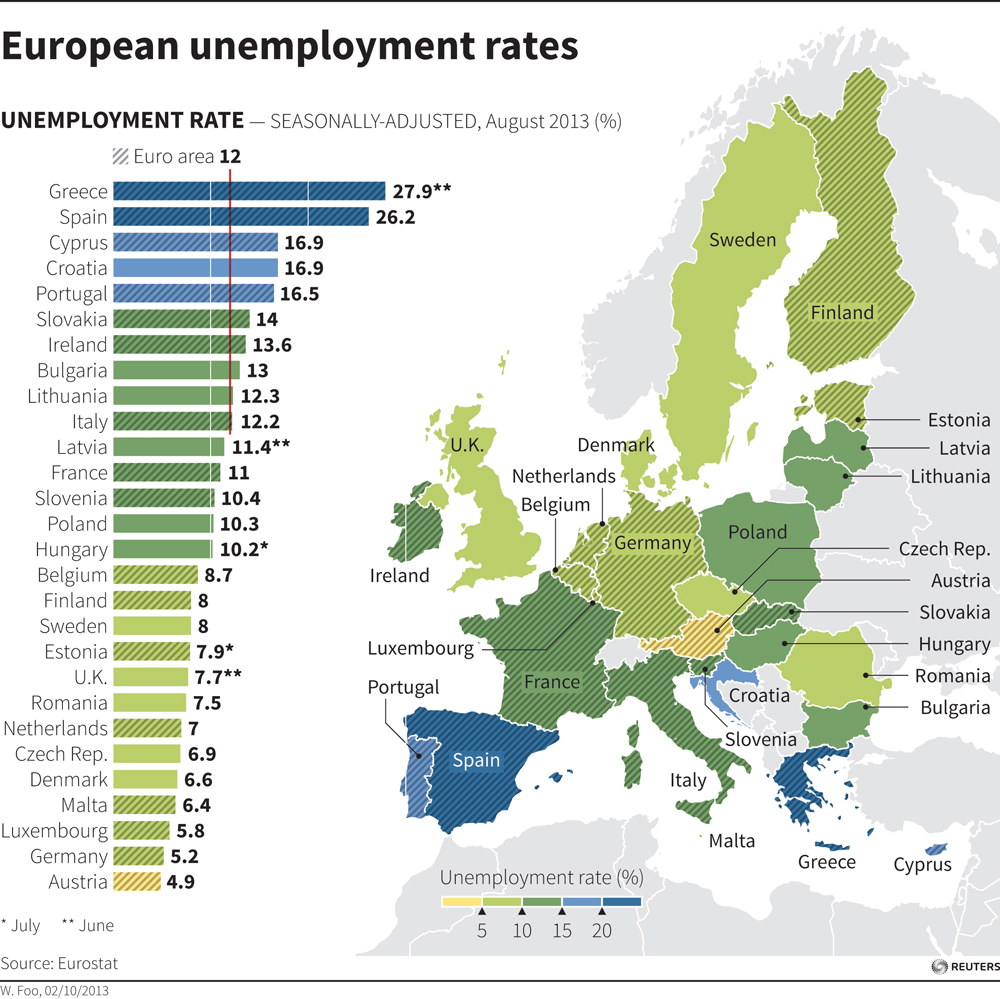

The PIIGS have extraordinarily high unemployment rates (27.9 percent in Greece, 26.2 percent in Spain, 16.5 percent in Portugal, 13.6 percent in Ireland and 12.2 percent in Italy). The ratios of debt to gross domestic product are also unpleasant: 147 percent in Greece, 109 percent in Italy, 87 percent in Portugal, 61 percent in Ireland and 51 percent in Spain. By contrast, Germany has an unemployment rate of 5.2 percent and a debt-to-G.D.P. ratio of 44 percent. Clearly the euro appears to be a union that was not made in heaven. Like Maria in the Austrian convent, is it time for some or all of the PIIGS to part ways and explore other options?

Benefits and Hazards

The euro was the project of President François Mitterrand of France and Chancellor Helmut Kohl of Germany in the 1990s to enhance political cohesion in Europe and further the process of economic integration begun with the creation of the Common Market by the Treaty of Rome in 1957.

The argument for the monetary union was enhanced price competition, since goods and services would be priced in a single currency, which in turn would lead to greater transparency about relative costs across borders, thus increasing the efficiency of making financial decisions. All of this, the countries hoped, would pave the way, in the medium-to-long term, toward greater convergence in economic growth and performance across the euro zone.

The individual governments, of course, would surrender their own independent monetary authorities, so there would no longer be the option of currency devaluation to regain competitiveness, relative to other countries, for marketing exports and capturing tourism. But even this, by the late 1990s, was not seen as a high price to pay. Too often, as in the case of Italy, an independent central bank just meant high and unstable inflation rates.

The euro zone is what is known as a currency area. Independent nations share a common currency but still have their own independent fiscal policies for government spending and taxation. Because the countries use common currencies, debt is denominated in that currency. So each country can issue debt in the same currency as the other countries of the currency union. But individual countries do not have political accountability to the currency union about how they tax and spend and thus run up their debt.

This combination of complete monetary union with little or no fiscal coordination or accountability is the Achilles’ heel of the euro zone. In the United States, for example, individual states do not have the power to issue their own currency and set exchange rates against the currencies of other states. But they are part of a broader federal tax and transfer system. In the wake of a natural disaster or economic downturn, for example, a state cannot devalue the dollar to encourage more tourism or investment, but it can receive federal transfers. Similarly, the federal government can mandate conditions for state spending or taxation in order for federal aid to continue.

This is not the case in the euro zone. Whatever bailouts have come so far to the PIIGS have come after long and contentious deliberation among the key players: the International Monetary Fund, the European Central Bank and the European Commission. These three entities are known, not so affectionately, as the troika in the PIIGS.

But the combination of monetary union without fiscal coordination is not the only Achilles’ heel of the euro zone. The European Central Bank is the monetary authority of the entire euro zone. One of the major responsibilities of a central bank is to be a lender of last resort to banks. If banks are in danger of a collapse, the central bank has the option of providing emergency financing. The reason for this mechanism is to prevent an individual bank crisis from turning into a systemwide financial panic through contagion effects. After all, if one well-established bank collapses, depositors at other banks may worry and withdraw their deposits, starting a general run on the banking system. As we know from earlier generations who lived through the Great Depression, a systemwide run on the banking system is not a pleasant experience.

Given that the European Central Bank has to function as a lender of last resort to member banks in the euro zone, one would assume this entity would have supervisory authority over these banks. In the United States, the Federal Reserve System is a lender of last resort, to be sure, but has supervisory authority over member banks through its 12 regional Federal Reserve Banks, and through the Office of Comptroller of the Currency and the Federal Deposit Insurance Commission. There is also a national uniform system of bank-reporting laws and a unified financial accounting framework.

None of this is true in the euro zone. While the European Central Bank has the responsibility to be a lender of last resort to the banks in the euro zone, each country has its own banking supervision laws and its own national accounting practices. The national central banks of the system, like the Bank of Portugal, the Central Bank of Ireland and the Bank of Spain, have responsibility for bank supervision in their respective countries, but it is the European Central Bank that has to serve as a lender of last resort in a time of crisis.

It should not be surprising that things have turned out the way they have. National governments like Portugal’s were able to run up large public-sector deficits while issuing euro-denominated bonds at low interest rates (since there was no longer any risk of a currency devaluation). At the same time, many banks throughout the system engaged in questionable lending practices, with less than adequate supervision from their national authorities, which no longer had the responsibility to function as lenders of last resort. In hindsight, it is easy to see that the adoption of the euro was premature for many countries in Europe.

Lessons From U.S. History

Many commentators have been advocating that their countries leave the euro and re-adopt their own national currency. The call is for a partial or full breakup of the euro system, with perhaps only a few countries retaining the euro.

The problem with the breakup of a monetary union of independent national states is that we have little data to indicate where this process of disintegration or fragmentation might end. Previous breakups of monetary unions took place in the context of nation-states breaking up, for example, in Yugoslavia, the Soviet Republics and the Czech Republic with Slovakia.

What happens if Spain, Ireland, Italy, Greece and Portugal start issuing their own currencies again? There will certainly be competitive devaluations against one another, leading to higher national inflation rates. But will things end there? Likely there will be trade restrictions, tariffs and controls on investment and labor mobility. With a currency breakup, Europe could regress to the state of affairs prior to the Treaty of Rome. As the Great Depression showed, increasing economic isolationism and protectionism is a sure way to prolong stagnation and delay recovery.

The other option is to enhance and strengthen fiscal consolidation through centralized control on taxation and spending across the member countries of the euro zone.

Thomas J. Sargent, a Nobel laureate and professor at New York University, has drawn a lucid comparison of the United States operating under the Articles of Confederation and the present euro zone. What triggered the adoption of the current U.S. Constitution in 1789 was a debt crisis. Before that the United States was a loose confederation of states with a common currency and a chief executive with little authority. The Northern states had accumulated large debts during the Revolutionary War, while the Southern states, rich in cash from exporting cotton and tobacco, had little or no outstanding debt from the war.

The issue for the new United States was the consequence of a default by the Northern states. Such a default would have repercussions throughout the country, making it harder for both Northern and Southern states to borrow internationally for capital equipment for infrastructure. Rather than risk the consequences of a default by the North, which would cripple the ability of the South to borrow internationally, the South agreed to federalize the war debts of the Northern states in exchange for moving the capital from New York to a new federal city in the South, Washington, D.C., and for greater centralized control over the collection of tax revenue and spending by states.

Europe is in a similar position today. If there is a breakup of the euro zone, there is a real chance that several of the highly indebted countries would not only devalue their new currencies but also default on the euro-denominated debt they hold. Since many banks throughout the entire euro region hold debt instruments from these countries, such a default would put considerable stress on financial institutions throughout the euro region. Like the South after the Revolutionary War, many countries would rather not see a default by the highly indebted countries in their currency union.

What to Do?

Although a breakup of the euro area is not out of the question, the better strategy would be to move forward and maintain the euro with a system of greater fiscal centralization. Clearly the European Central Bank has to harmonize bank accounting and regulatory standards across the system. For the euro to work, national governments will have to yield some—though by no means all—of their fiscal autonomy to a centralized Ministry of Finance in the euro system, much the way state governments have citizens paying direct and indirect taxes to the federal government.

Finally, there is the question of the way money moves across borders in the euro zone and beyond. The roots of the euro-zone crisis lie in the all-too-human tendency to borrow too much in good times, when lenders are exuberant, and in bad times to fall into situations of bankruptcy and severe recession as lenders become excessively risk-averse while investment dries up and unemployment skyrockets.

We are moving into the age of macro-prudential regulation, which calls for new, nontraditional tools of stabilization, so that we will not fall into this type of crisis in the future. In good times, when markets become overly exuberant, taxes on the flow of international capital can help moderate the accumulation of large amounts of debt and in bad times, when lenders are risk averse, subsidies for new lending would generate funds for new investment opportunities. As the late James Tobin of Yale would probably advocate: the time has come to throw some sand into the highly lubricated gears of the financial system.

The euro was a bold initiative, to be sure, but the painful experience of the last five years has shown how vulnerable the overall structure was. Just as the United States learned lessons from the weaknesses of the Articles of Confederation, so the euro zone can learn from the present crisis and move forward toward greater integration in fiscal policy to support the monetary union, as well as to create some helpful frictions in the borrowing and lending taking place across member-state borders.

While the learning and restructuring process will be long and difficult, a euro breakup risks putting Europe in a back-to-the-future mode, reverting to the isolationist days before the Treaty of Rome.